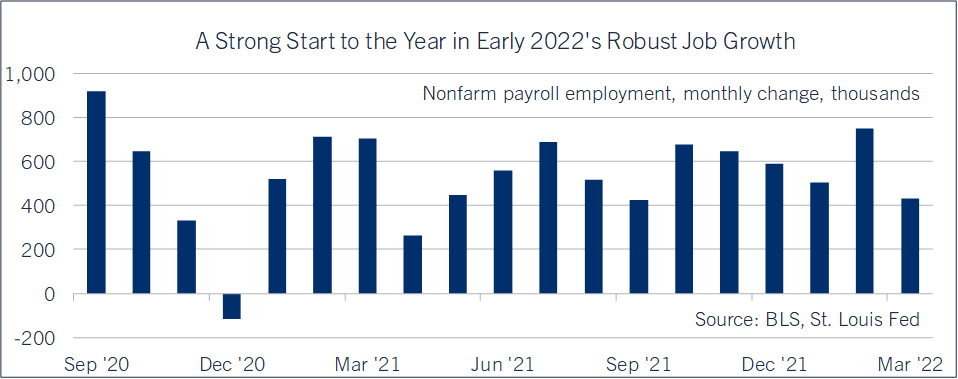

The jobs report was solid all around, with good monthly job growth, upward revisions to January and February, and a bigger-than-expected drop in the unemployment rate. Employers added 431,000 nonfarm jobs to payrolls in March, undershooting the consensus forecast of 490,000; Comerica had forecast 500,000. But payroll job growth in January and February was revised up by a net 95,000 jobs, so the net increase in jobs in March versus the prior jobs report (including both jobs added and revisions) was a robust 526,000.

March saw solid job growth in goods-producing industries, including 38,000 more manufacturing jobs (of which 6,000 were in motor vehicle and parts manufacturing). Construction employment rose 19,000 and mining employment rose 2,000. Private services-providing industries added 366,000 jobs, including 112,000 more leisure and hospitality jobs, 102,000 more professional and business service jobs, 53,000 more education and health service jobs, and 49,000 more retail jobs. Public employment changed little on the month, up 5,000, with 16,000 more local education jobs mostly offset by dips in state education and non-education jobs.

The unemployment rate fell to 3.6% from 3.8% in February, beating market expectations and Comerica’s forecast for 3.7%. In the survey of households from which the unemployment rate is derived, employment surged 736,000 in March, the labor force (people employed or actively looking for work) rose 418,000, and the number unemployed fell 318,000. At 3.6%, the unemployment rate is within rounding error of late 2019 and early 2020’s half-century low of 3.5%. Other labor market indicators, like job openings and insured unemployment (total recipients of unemployment insurance benefits, reported weekly) are already stronger than before the pandemic.

Unemployment rates for demographic groups that historically lag in economic recoveries improved notably in March. The unemployment rate for Black or African Americans fell to 6.2% from 6.6% in February, and was down from 9.5% in March 2021. The unemployment rate for Hispanic or Latino Americans fell to 4.2% from 4.4% and was down from 7.7% a year earlier. Like the overall unemployment rate, the unemployment rates for both Black and Hispanic Americans are closing in on their pre-crisis lows. The unemployment rate for men ages 20+ fell 0.1% to 3.4%, and the rate for women ages 20+ fell 0.3% to 3.3%.

The labor force participation rate rose to 62.4% from 62.3% in February. It was over 63% prior to the pandemic, meaning labor force participation is still about 2.5 million below the pre-crisis level, of which about a million are early retirements.

Average hourly earnings rose 0.4%, matching the consensus forecast, and were up 5.6% from a year earlier after a 5.2% increase in February (revised from 5.1% previously). Average hourly earnings are lagging inflation, dampening consumer sentiment in recent months. Average weekly hours of private workers dipped to 34.1 in March from 34.2 in February; strong job gains in industries with more part-time workers like leisure and hospitality and retail contributed to March’s shorter average workweek.

Robust job growth in the March report will stiffen the Fed’s resolve to normalize monetary policy in a hurry. Comerica Economics forecasts for the Fed to raise the federal funds rate by half a percentage point at both of their next two meetings, in early May and mid-June. In the first quarter of 2022, monthly payroll job growth averaged a robust 562,000, a 4.6% annualized rate. This means that a soft GDP report for the first quarter (The consensus forecast is for 1.5% seasonally-adjusted and annualized) shouldn’t discourage too much. Real GDP will not capture the strength of the economy’s recovery in early 2022.

While the U.S. economy had excellent momentum in early 2022, the outlook has darkened due to the Russia-Ukraine war and the surge in energy and food prices it has caused. Another jump in consumer prices, and to a lesser extent the drag on exports, will weigh on the recovery in the rest of the year, and cautions against extrapolating from early 2022’s trend.

Comerica forecasts for average monthly payroll job growth to slow to 455,000 in the second quarter from 562,000 in the first quarter, as discretionary consumer spending growth slows amid the Russia-Ukraine shock. The unemployment rate’s decline is likely to stall for a while. As financial pressures from inflation mount, more Americans who exited the labor force during the pandemic can be expected to re-enter, fueling faster labor force growth and keeping the level of unemployment largely steady (the government defines unemployment as people who don’t have a job and actively searched for one in the prior four weeks).

Bill Adams is senior vice president and chief economist at Comerica.