• New single-family home sales dropped 17% in April as higher mortgage rates shocked the market.

• Inventories of new homes are rising, though still pretty tight.

• House price increases will slow as higher interest rates constrain demand and supply rises.

• As house prices rise more slowly, overall inflation will cool as well.

The extreme seller’s market in housing is turning. New single-family house sales dropped 16.6% to 591,000 at an annual rate in April from a downwardly-revised 709,000 in March, which was marked down from 763,000 in the prior release. Combining revisions with the monthly drop, new house sales were down more than 20% from the level originally reported for March. Ouch! Existing home sales also fell in the month, though not as hard. They were down 2.4% to a 5.61 million annualized rate, from 5.75 million annualized in March (revised down a hair from 5.77 million previously). New home sales were down 26.9% on the year and existing home sales down 5.9%. Their drop is largely due to higher mortgage rates. The average rate for a 30-year mortgage rose more than two full percentage points between the end of 2021 and the end of April, according to Freddie Mac’s national survey of lenders.

Inventories are rising but still tight. The number of new houses for sale rose to 444,000 in April, the highest since mid-2008, but nine in ten listings are for houses under construction or not yet started—to state the obvious, that is less attractive to buyers with immediate housing needs. The share of completed homes in total listings was the smallest since comparable data began in 1999, reinforcing how dysfunctional the housing supply chain still is. Listings of existing homes are extremely tight. April’s 1.03 million listings were equivalent to 2.2 months’ supply at the current sales pace, slightly lower than in April 2021, when there were 2.3 months’ supply listed.

With pending home sales (houses going under contract) down 3.9% on the month in April, home sales are likely to head lower near-term before stabilizing in the second half of 2022. Early this year, listings were swamped with multiple offers across much of the country, but the sudden jump in mortgage rates has thrown many homebuyers’ plans into disarray. Some of the buyers who had to go back to the drawing board as interest rates rose will adjust, draw up more modest budgets, and return to the market. This will help home sales to stabilize. But with house prices and interest rates much higher than pre-pandemic, there are simply fewer Americans who can afford homeownership. This, along with more finished new homes coming to market as homebuilders get past their supply chain problems, will bring the extreme seller’s market in housing back toward balance.

Seeing the writing on the wall, homebuilders are shifting activity to the multifamily segment. Multifamily housing starts rose to 612,000 annualized units in April from 524,000 in March and were the highest since 1986. Single-family starts fell to the lowest since last October in April. Overall housing starts edged down 0.2% on the month in April, with the March level revised down a big 3.6% from the prior report.

In another sign of how higher interest rates are cooling the housing market, price increases are finally starting to moderate. The year-over-year increase in the median sale price of a new single-family home slowed to 19.6% in April from 21.0% in March (though median prices were still up sharply in the month, to $450,600 from $435,000). The year-over-year increase in a median existing home’s price slowed to 14.8% in April from 14.9% in March and 15.7% in February—and was up 4.4% on the month (not seasonally-adjusted) to $391,200.

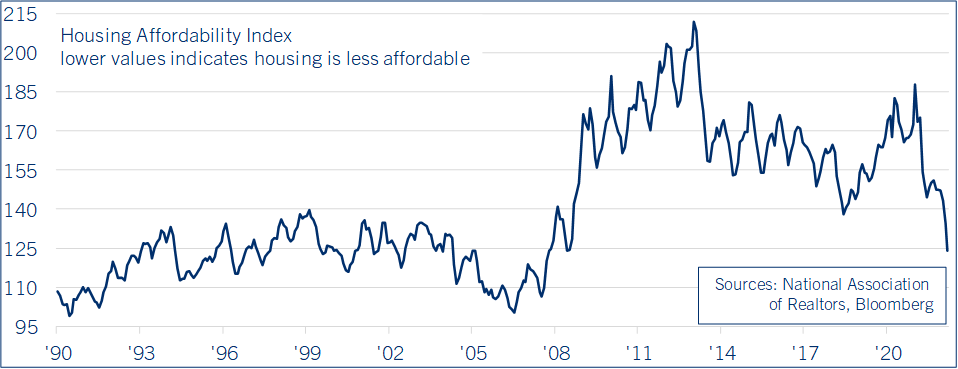

Big changes in monetary policy are behind this housing slowdown. Last fall the Federal Reserve started to pivot from a crisis-fighting footing toward a neutral or even tight policy, as their focus shifted from fostering a recovery to fighting inflation. Mortgage interest rates jumped as the Fed ended purchases of Treasuries and mortgage-backed securities, raised short-term interest rates, and signaled they would start shrinking their holdings of securities in June. The combination of higher interest rates and much higher housing prices than prior to the pandemic has made homeownership much less affordable. The National Association of Realtors’ Housing Affordability Index, which takes into account household incomes, mortgage rates, and house prices, shows that homeownership is the most expensive for a typical American household since 2008 (See chart).

Home price increases will continue to slow as the housing market normalizes further, but an outright decline in prices looks unlikely. While monetary policy is a headwind for housing, end demand is higher than before the pandemic because of the rise of remote work and other lifestyle changes. This is a big support to the housing market. It is also the flip side of continued depressed demand for office space. On top of this, the strength of the job market, and much more conservative mortgage underwriting than in the mid-2000s’ housing bubble, should help housing adjust to higher mortgage rates.

Comerica Economics forecasts for the S&P CoreLogic Case-Shiller National House Price Index to slow from nearly 20% in year-over-year terms in February to 10% at the end of 2022, and to 2% at the end of 2023. With the labor market expected to stay tight, house prices are set to increase more slowly than wages next year. Slower house price increases will go a long way to cool inflation, since shelter accounts for about a third of the CPI index.

Bill Adams is senior vice president and chief economist at Comerica.